Did you know compound interest can boost your savings potential?

21 April 2021

Share this article

Did you know there are two types of interest – simple and compound?

We all love getting interest on our savings, but getting compound interest is even better. In this article, you’ll learn what compound interest is, how it’s calculated and how you can take advantage of it.

What you'll learn

- The difference between compound and simple interest.

- How to calculate compound interest.

- Why you could take advantage of savings accounts with compound interest.

What is interest?

Interest is money you earn on your savings when you put them in an interest-earning account. How much you earn depends on the interest rate offered by the bank or building society you choose to save with, and the length of time you leave your money in that account.

The interest rate you're on affects how much you earn on your savings. The higher the interest rate, the more money you'll earn and accumulate over time, so it has a significant impact on your savings.

However, it’s important to remember that interest rates can rise and fall because, in the UK, they are influenced in part by the fluctiations in the Bank of England base rate.

What does simple interest mean?

Simple interest is an easy concept to get your head around. If you place £500 into a savings account for a year at a simple interest rate of 5% AER (fixed), by the end of the year, you’ll receive £25 in interest, bringing your balance to £525.

In other words, simple interest is based on the principal amount of your deposit.

What does compound interest mean?

When we’re talking compound interest, things get, well, interesting.

Essentially, compound interest is based on the original amount you deposit, plus the accumulated interest of previous periods. You get interest on interest, and it helps your savings grow faster.

How to calculate compound interest

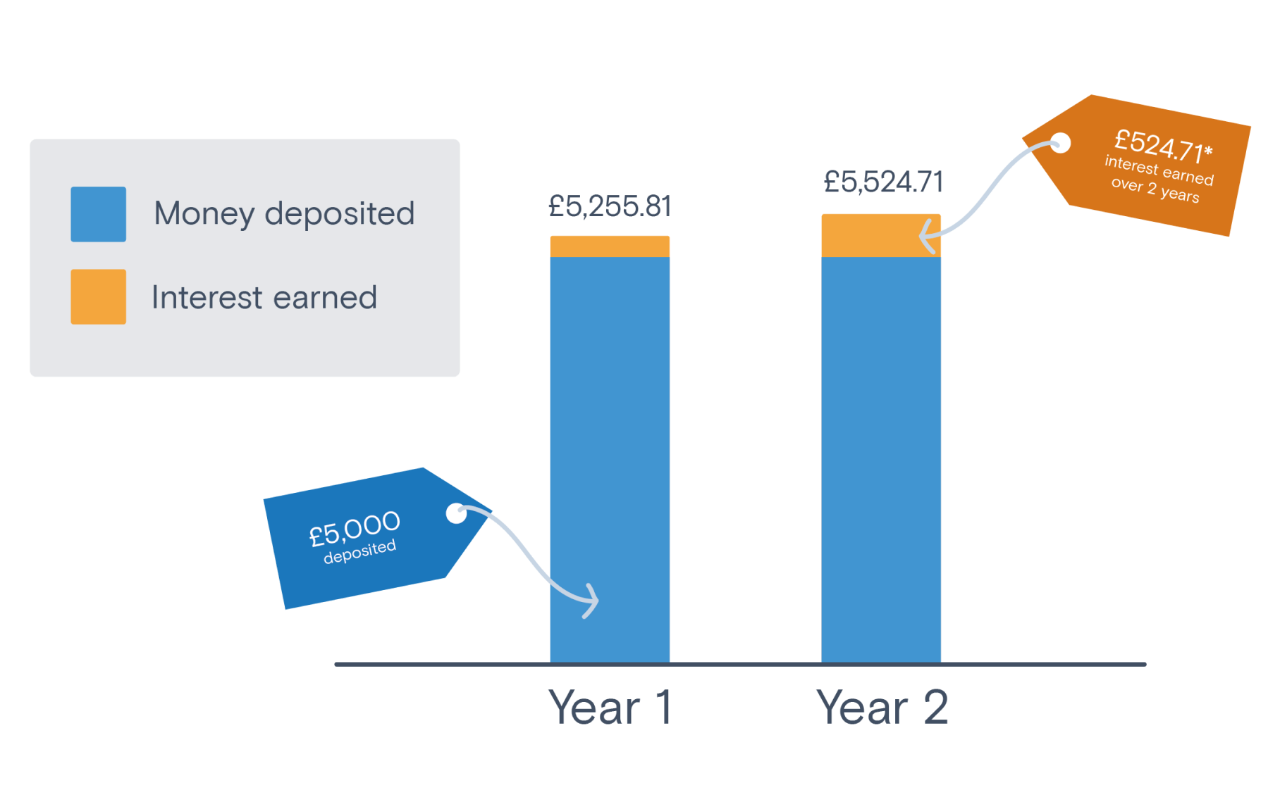

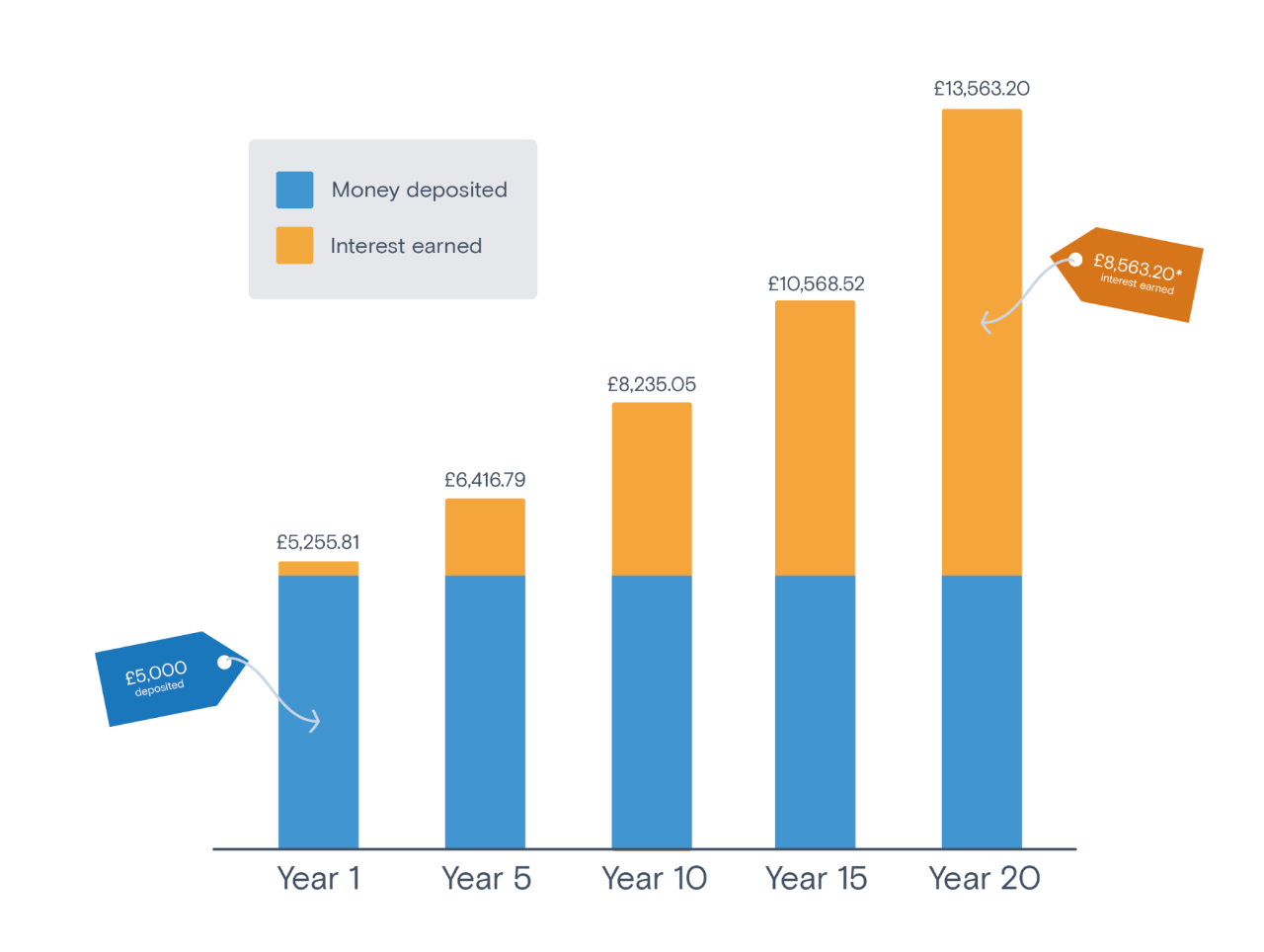

Let’s say you saved £5,000 in an account with an interest rate of 5% AER (fixed), with interest being paid into your account each month. At the end of the first year, you’d have £5,255.81* after earning £255.81 in interest.

At the end of the second year, you’d have £5,524.71*– that’s £268.90 in interest this year – because you would have earned interest on both your original savings and the interest you earned monthly from last year.

Why it pays to start early

Where compounding really gets exciting is when you put your savings away for a longer stretch of time. If you left your money where it was for 20 years at the same fixed interest rate and let compounding work its magic, you’d earn a total of £8,563.20 in interest and be left with a balance of £13,563.20*.

All without you paying in another penny.

*Based on a fixed interest rate of 5% AER. These projections assume you make no withdrawals or further deposits other than those mentioned that the interest rate doesn’t change and that interest is paid monthly into the account. It’s for illustrative purposes only and doesn’t take into account individual circumstances.

AER stands for Annual Equivalent Rate and illustrates what the rate would be if interest was paid and compounded once each year.

The content in this article is for information only and is not advice. All content in this article was accurate on the date of publication shown above.

Related articles

Connect with us on social media

Follow us on social media for news, insights and tips from Marcus by Goldman Sachs.